Under the logic of this theory it was imperative to intercede – but the obvious issue became how would one know what constituted a domino tall enough that when tipped over it’d begin an inexorable chain reaction? Communist guerilla campaigns within a country? Communist quasi-sovereign zones within a country? Somewhat ambiguous groups within a country with outside communist funding? What’s the threshold? When was intervention warranted, and if intervention came after the domino tipped and the chain reaction began then what?

There were many conflicting views over how Incora would flesh out – although as I mentioned months ago, Judge Isgur wasn’t holding his cards too close to his chest on his leanings – but what no one had on their bingo card was an invocation of the domino theory retrofitted for a certain kind of uptier (or, perhaps better said, a certain way to enable liability management exercises writ large to occur – uptier or otherwise).

Judge Isgur is soon departing the Southern District of Texas’ complex panel, and as he does so his parting gift is a loose theory around “domino” agreements that will lead to a series of quagmires. Because, once again, the issue becomes what constitutes a domino tall enough to begin an unstoppable chain reaction?

While I wasn’t a fan of a few aspects of how Judge Isgur handled Incora’s trial – as I alluded to in a prior post regarding the cross-examination of an advisor to the Participating Noteholders – and this whole process has taken far too long, there are few who could listen to the trial, or his monologues from the bench, and not be impressed at his patience (with some notable exceptions) and the complete sincerity in his approach (even if almost everyone he tried to help through his novel theorizing weren’t appreciative of it).

I should also mention that while I don’t agree with the outcome of Incora as it stands now (as I’ve said many times before, my biases are nothing if not well advertised), the written opinion that’ll (hopefully!) be a bit more fleshed out hasn’t been released and there are still some known unknowns (to co-opt another more recent foreign policy adage).

If Judge Isgur believes in a very narrow version of what constitutes a so-called “domino agreement”, then sure, fine, whatever. As I try to articulate below, if that very narrow version is all that’s operative then it’s a decision of little consequence to uptiers overall – but one that eviscerates Silver Point and Pimco’s new-money contribution in this case because they dotted their i’s and crossed their t’s prematurely (due to logistical ease, not malice).

However, if the view of Judge Isgur (which he hasn’t made too clear) is that there would be an issue here even if not for the automaticity discussed in the oral ruling – or rather if his definition of automaticity encompasses any series of events that seem somewhat automatic on balance – then his domino digressions will lead to a set of absurd quagmires if adopted by others. And it seems that he may be disposed toward this broader definition of automaticity because of a misconception over the economic calculus that a distressed fund operates under in a setup like Incora’s.

In other words, even though automaticity may be the right way to characterize how Incora was able to complete its 2022 uptier, it’s not axiomatic that the automaticity was required (it was a nice to have, not a need to have). Nevertheless, this appears to be the heart of the oral ruling: there was automaticity because there had to be automaticity. But that’s not the case.

Note: Not for the last time, the rough IC memos of distressed groups are coming back to bite them – everyone should know by now that in LMEs the audience should extend beyond the IC itself, and should be written accordingly (lots of footnotes on downside risks, whether modeled or not)...

Note: This was written in the aftermath of the oral ruling, and as such is a bit of a navel-gazing exercise. Since the content of the status conference on August 13 isn’t public knowledge, it won’t be discussed here (although it was a continuation of the theme of confusion that permeated the close of Incora’s trial and Judge Isgur’s oral ruling vis-à-vis the treatment of the $250mm injected by Silver Point and Pimco). Those with upcoming interviews should focus their time on actual interview-related stuff, and not on my airing of grievances (some of which may be unwound by a written opinion that hits the right notes – that opinion, which will cement and perhaps clarify aspects of the oral ruling discussed below, should come any day now...).

An Interlude on Incora and Uptiers

One of the themes that you may or may not have picked up in my writing over the last year is how irritated I’ve been over what I’ll call the presumption of permissibility – the notion that because there are precedent transactions that haven’t been unwound, that one can then stretch the bounds even further and that, if one’s transaction is found impermissible, only the aspects of the transaction that pushed the bounds will be unwound in some manner.

However, this all rests on the assumption that there will never be a court – inclusive of an Article III court – that will look at a transaction in toto, find it offensive to their sensibilities, not realize the implications of a full unwind, and set us up for an absolute mess.

In other words, some seem to operate under the presumption that uptiers reside on some kind of solid bedrock and that, at worst, transactions that stretch the bounds will be rolled back to some kind of normalized uptier formulation. This is a dangerous gamble, and one that to-date has largely relied on the reputation of the Southern District of Texas as being receptive to these kinds of transactions.

But remember that Serta is still at the Fifth Circuit – the trial occurred last month – and due to the fallout from Judge Jones’ unfortunate downfall and its reverberations, it’s at best not a favorable backdrop for uptiers right now.

The last time we talked I discussed how this idea has been internalized by funds and their advisors and there has been a response toward uptiers becoming less aggressive this year with the value shifts that are occurring being more in line with reasonable indirect compensation for the risks undertaken by participating creditors. And, as a result, we’ve seem limited to no litigation over the uptiers that have occurred as of late.

In Incora and Robertshaw – both of which have had narrow, transaction-specific setbacks from a participating creditor’s perspective over the last month – we’ve seen Judge Isgur and Judge Lopez, respectively, walk a delicate tight rope in order to uphold uptiers as a concept while overturning some more aggressive maneuvers around them.

So, even though Silver Point and Pimco don’t feel like Judge Isgur has done them any favors, and Invesco doesn’t feel that Judge Lopez has done them enough of a favor, both opinions are fine – and there should be more of an appreciation of this fact.

In truth, Incora and Robertshaw were never supposed to end up as they did. They are both the result of transactions that started with a clean, solid premise; ended up being bungled in their execution; involved participants scrambling to retain value, rolling the dice that future litigation would be favorable to them because they had no other option; and thus opened up the possibility of uptiers writ large being attacked if these cases happened to land in front of ill-disposed judges.

The machinations of Incora and Robertshaw are understandable from the participating creditors perspectives – they did what they needed to do to preserve value when their transactions went sideways, and it’s all logical enough. But they’re both doing the already small minority of those that support these transactions no favors.

There’s been a lot of talk about how developments in Incora – or, to a lesser degree, Robertshaw – have ushered in some sea change vis-à-vis uptiers or even liability management exercises writ large. That Incora’s result is somehow the end of uptiers. This isn’t the case at all, and it’s bizarre that the public commentary is so divorced from reality.

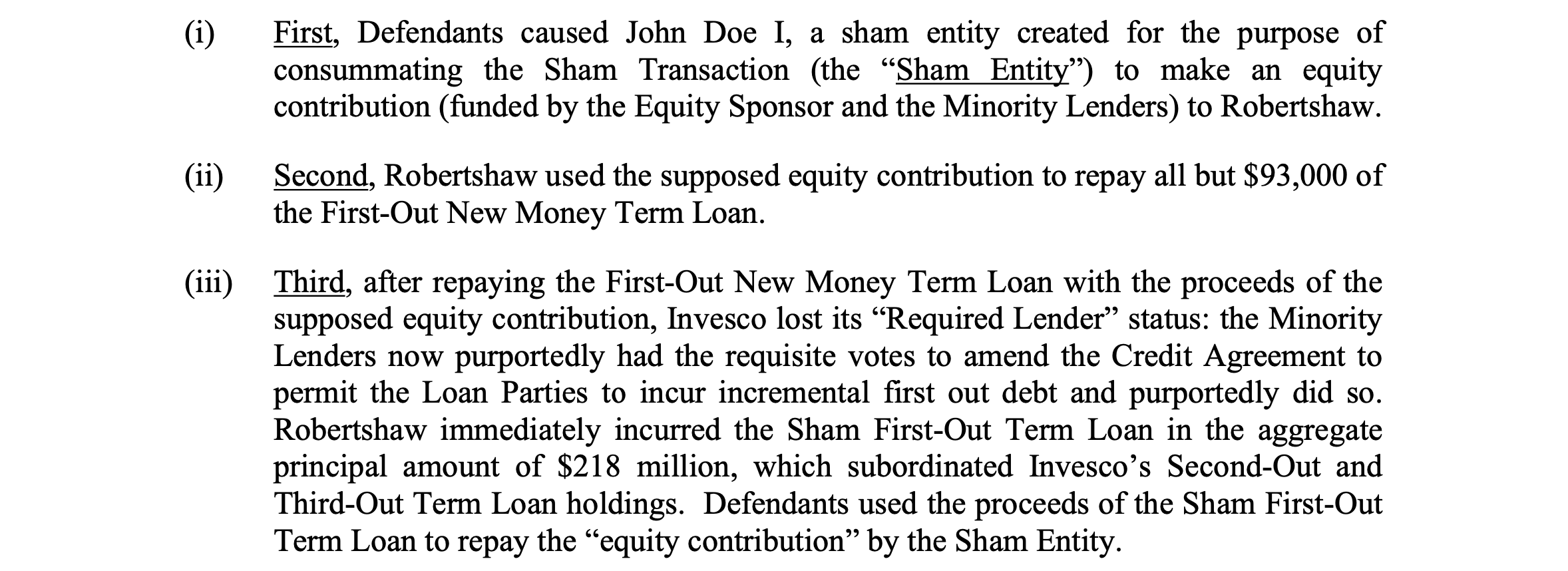

The core of both transactions were explicitly upheld without much affair. What was rolled back were the aggressive maneuvers that were made after the transactions were bungled and a mad dash occurred (in the case of Incora for Silver Point and Pimco to reach a supermajority in the 2026 Notes, in the case of Robertshaw for Canyon, Bain, and Eaton Vance to regain Required Lender status again after Invesco’s initial shenanigans).

Both of these opinions are, in their own ways, a pushback against aggressive maneuvers, I suppose. But both do not touch the core of what is a non-pro rata uptier. Rather, they touch the way one can end up in a position to effectuate one.

Even this is a statement too far – because neither decision lays down some kind of broad prohibition on how one can build up (read: manufacture) a position that allows one to reach the required consent threshold to effectuate a non-pro rata transaction. Rather, both Judge Isgur and Judge Lopez found small technical issues within the docs that are non-universal (e.g., not found in all docs) that in these specific cases made some specific actions by these funds unauthorized – and as such, the roadmap for manufacturing a certain position while not falling afoul of the logic used in these decisions is simple enough (even though, of course, in most instances no manufacturing is needed since participants “organically” hold the required level of consent to begin with).

Rest assured, uptiers as a concept have lived to see another day. But this is because Judge Lopez and Judge Isgur wanted them to live another day. There should be some appreciation of this, and that uptiers still rest on a fraught foundation.

Incora’s Trial and Tribulations

Back in 2022, when the litigation over Incora’s transaction kicked off, I wrote a few long posts that detailed the mechanics of the transaction itself, so there’s no reason to relitigate that here too much as it’s pretty straightforward.

Indeed, much of what’s happened over the last few years has been an exercise is rehashing the same talking points with different emphasis and in different venues – not a bad deal for those that bill by the hour, I suppose.

So, what I want to do is talk through the oral ruling from Judge Isgur, how it was arrived at, and the broader implications because I think it has been both misunderstood and mischaracterized.

I disagree with the ultimate outcome on Incora’s core uptier issue (surprise, surprise) but overall am nonplused about its broader ramifications – and it’s been a surprise to see how many have called this some kind of death nail for uptiers.

The concern that folks should have vis-à-vis the ruling is in how it was arrived at, and what exactly constitutes a so-called “domino agreement”. Although this is partly an intellectual exercise because i) there are few uptiers where there is something that approximates a so-called “dominion agreement” in this context and ii) this isn’t liable to be the lens that other judges view uptiers that are similar in nature through.

So, to be clear, there’s not a whole lot of utility to this post for most readers, and for the sake of time I’m going to assume a lot of background knowledge about the case. But this is my venue for venting, and I want to vent about Incora, so you’re getting 12,000 words on it and them’s the breaks.

After a month’s long trial – in which Judge Isgur’s normally dispassionate disposition revealed he wasn’t too disposed to Silver Point, Pimco, or Evercore as their advisor – on June 26th we were subjected to ninety minutes of confusion by all parties, consternation by Judge Isgur who didn’t understand why everyone couldn’t read between the lines vis-à-vis his views, and finally capitulation by counsel to Silver Point and Pimco after recognizing that they had lost – and lost in a far more profound way than they ever imaged they could lose.

To suggest the June 26th hearing wasn’t what anyone expected – because it was so detached from what was being argued in closing arguments on June 24th and 25th – would be an understatement.

Because what everyone thought was that the purpose of this hearing was to discuss – assuming that the uptier was impermissible – if the Non-Participating Noteholders would be entitled to the restoration of their liens as they existed prior to the uptier. The debtor (Incora) and Participating Noteholders both argued that this could be the case, but since this would be a form of equitable, not legal, relief the requirements for pursuing an equitable lien, or equitable subordination under 510(c) of the Code, must be met and they aren’t here because, in part, the transaction was clearly done in good faith. Meanwhile, the Non-Participating Noteholders believed that pursuing an equitable lien, equitable subordination, etc. was all possible here and also argued separately that a restoration could constitute a form of legal relief (basically telling Judge Isgur, “Pick your poison, but restore our original lien status.”).

Anyway, all that doesn’t matter too much (read the post-trial briefs if you want all the details on how Participating Noteholders and Non-Participating Noteholders framed what they thought Judge Isgur could do) because Judge Isgur had his own ideas – including on what legal and equitable relief mean – and it took a while before everyone could appreciate what those ideas were...

The hearing on the 26th began with a disorienting back-and-forth between Judge Isgur and Rosenbaum (counsel to the vast majority of the Non-Participating Noteholders, and someone who has done a pretty masterful job through Incora’s saga) in which Judge Isgur explained that he created a “complicated” Excel model (oh, no) and was trying to model out a retrospective pro-rata transaction (double oh, no).

In other words, a transaction where the ~$250mm that Silver Point and Pimco injected for the new 2026 Notes, at par, would have been open to everyone to participate in. So, we’d forget the uptier ever happened and the amount of the 2026 Notes held by Incora and Silver Point for Plan purposes would be their holdings before the transaction which were around ~59%, the Non-Participating Noteholders would have the remaining ~41%, and then a series of “adjustments” would be made to figure out the “fair” amount of recovery (read: percentage of the class) for everyone.

For example, Judge Isgur said he would “charge” the Non-Participating Noteholders with the pro-rata cost of putting in their share of the ~$250mm – not in literal cash, of course, but in terms of what their entitled to from a Plan distribution perspective because Silver Point and Pimco really did put in ~$250mm of cash, so they need to get some amount back or, put differently, Non-Participating Noteholders would need to give up some of their share of the distribution pie to Silver Point and Pimco based on the fact they put in all the cash.

This then began a confused back and forth over what adjustments should feed into this model, and in this back-and-forth Rosenbaum had an all-time great line vis-à-vis Judge Isgur’s retrospective recap model, “So, so, so, we, right, if you’re thinking columns or debits and credits, whatever, there’s no question you’re better with spreadsheets than me, but I can think of debits and credits.” (Take note: the best way to obfuscate obsequiousness is to ground your pandering in truth.)

This obsequiousness of Rosenbaum was because he thought he and Judge Isgur were on the same page and he was about to get exactly what he wanted: a restoration of the 2026 liens that were stripped through the Fourth Supplemental Indenture (that allowed for the subsequent uptier of Silver Point and Pimco’s 2024 and 2026 Notes).

But then it seems that Rosenbaum began to internalize what this model really involved as Judge Isgur began poking at the idea that maybe he has the authority to temper what he considered legal relief (the restoration of the liens of the Non-Participating 2026 Noteholders) through equitable relief to the benefit of Silver Point and Pimco (via giving them something, other than a worthless unsecured claim, for their ~$250mm contribution such as equal lien status and downward adjustments to the Non-Participating Noteholders to account for the fact that Silver Point and Pimco, like, were the ones who actually provided all the cash, that cash led to interest payments to the benefit of all noteholders that wouldn’t have come otherwise, etc.).

Here's Judge Isgur: “Y’all [Non-Participating Noteholders] would have put in your share of the money, right? So, if I’m going to then elevate them [Silver Point and Pimco] to your level, I need to give them back the share of money they put in that rightfully... that you would have put in in a hypothetical scenario. That’s why this isn’t a legal remedy. This is sort of the 510 granddaddy Pepper V. Litton of saying, do your best to do justice. But justice isn’t one sided here, because they put in a huge amount of money desperately needed by the debtor, and it was the only alternative.”

In the end, the way that Judge Isgur views the issue of Incora’s core uptier is that there are two binary legal remedies that seem to be available sans a more creative maneuver on his end: one that overcompensates the 2026 Non-Participating Noteholders (via the restoration of their liens, but treating the ~$250mm in new-money from Silver Point and Pimco as a worthless unsecured claim) or one that undercompensates the 2026 Non-Participating Noteholders (via not restoring their liens and giving them an unsecured claim for the amount of their damages, which would be worthless and is what Silver Point, Pimco, and the debtor have argued is the only available option for Judge Isgur – regrettable as that is, wink wink).

Or in his words, “...should I pick under compensating you [the Non-Participating Noteholders] or overcompensating you in real life, by voiding or by preserving your lien, versus by giving you an unsecured claim? One overcompensates, one undercompensates. I don’t like either alternative...”

So, here’s Judge Isgur’s core question that no one was prepared to talk to, as illustrated by all the subsequent stuttering and stammering that occurred from $2,000/hr lawyers: “If it takes away some legal relief that you [the 2026 Non-Participating Noteholders] are entitled to, because if you’re telling me that I can take away some legal relief in fairness to you then I should be able to, by that some token, be able to take away some of your legal relief to do fairness to them [Silver Point and Pimco]. And my question is, do I have the authority to do that?”

Once again, this is kind of the inverse of what folks thought this hearing would be about: everyone thought it’d be about if the Non-Participating Notes could benefit from equitable relief if the transaction was found to be impermissible, not that the Participating Noteholders (a.k.a the wrongdoers) could.

So, Rosenbaum, like all others, basically said, “Uh, I don’t know? Where did this come from?” or to quote him directly, “I don’t think I can, at least on today’s record, I don’t think I can go that far, at least without further conferring with my clients,” and “...as much as we enjoyed the last few days, I think this is a whole other intellectual exercise that we need to wrap out minds around but, but...”

Since Rosenbaum was trying to figure out what was going on here in real time, he mistakenly revealed the biggest issue with equitable relief overall in these circumstances – no matter who it benefits. “In other words, it, it’s a dangerous game, right? In other words, if you’re going to come in and want… and this is the relevance to your other question, why I was mentioning the 64% [Pimco projected] IRR [if the transaction stands], I agree with you. You’re entitled to make money, make as much as you can, but with risk, it comes reward, but it also comes volatility. And if you’re going to take that much risk and it’s going to harm somebody else, then you… you should bear all the downside consequence [Silver Point and Pimco being left with an unsecured claim, and not having the benefit of the $250mm residing pari to the other 2026s with their now restored first liens]”.

What Rosenbaum is getting at here is the dangerous game of beginning to think about equitable remedies. What is fairness? What are the right retrospective adjustments to make? I’ve harped on this theme for years as I’ve warned that despite all the smoke and mirrors we’re going to end up having these cases decided based on abstract applications of fairness (even if dressed up in legal garb, perhaps through invoking a 1939 Supreme Court opinion like Pepper v. Litton) and that the jettisoning of this was the deceptive genius of Judge Jones’ opinion which casually disregarded it more or less due to his “financial titans engaged in winner-take-all battles” rationale.

If we start venturing down the equitable rabbit hole in this way – trying to reconfigure transactions for fairness years after they occurred – then the best way to do that is, of course, through creating retrospective recap models that back out “fair” IRRs for everyone involved (even though no one will be talking explicitly about IRRs).

But that, of course, is a near impossible feat as Judge Isgur admitted when he said there was a lot of inputs into his “model” that he hadn’t figured out yet when it came to how to adjust everyone’s stake in the 2026s (e.g., all the legal fees that are a direct result of Silver Point and Pimco pursuing the transaction that’s now deemed impermissible to begin with!).

So, what IRR should Silver Point and Pimco have on their ~$250mm of additional 2026 Notes when the raison d'etre for the issuance of those additional Notes, per Judge Isgur, was to enable the uptier which he has now deemed impermissible? What IRR should the Non-Participating Noteholders have when they did nothing wrong? What if they’re primed by a DIP with some nice fees provided by those that did them wrong, and the reason this DIP could be provided was arguably due to the wrongdoers’ elevated status in the capital structure as a consequence of the now impermissible uptier? But, also, should all Non-Participating Noteholders really be treated equally because Golden Gate bought hundreds of millions trying to get a blocking position leading up to the transaction and therefore weren’t some kind of innocent bystander? Should those that were truly innocent bystanders be treated better? What about the Non-Participating Holders of the 2024 Notes that Silver Point and Pimco did have a supermajority in before the transaction but who maybe wouldn’t have had their liens stripped if the original transaction didn’t occur?

Judge Isgur’s philosophizing had already been done, and he had no interest in hearing the equitable philosophizing of others. He had (for now) already made up his mind that he wanted to i) restore the liens of the 2026 Notes as they were pre-uptier (which would be to the benefit of not only the Non-Participating 2026 Noteholders but would also, of course, be to the benefit of Silver Point and Pimco since they held a simple, not super, majority of the 2026s pre-uptier) and ii) provide something more than a worthless unsecured claim to Silver Point and Pimco for the ~$250mm in new-money that came in through the additional 2026 Notes issuance since, like, that was real money (at par!) that provided real benefit (enhanced runway!) even though Judge Isgur thinks it was impermissible on its face (huh!).

So, Judge Isgur made it clear since he seemed bewildered that everyone still hadn’t appreciated what the point of this hearing was, “I’m not asking you what the equitable remedy ought to be. I’m asking you if I have the authority as the United States bankruptcy judge… to utilize Pepper V. Litton… to overcome legal relief.” (In other words, to use this 1939 Supreme Court decision to “…do justice to make things right” in a manner that no one has ever done before).

Next up – counsel for the debtor, Kirpalani – said the quiet part out loud, “…I’m going to be as blunt as I’ve ever been with you. I’m not sure exactly what we are discussing, because what your honor described a little while ago as a legal doctrine in your mind, to me, is an equitable doctrine.” In other words, the restoration of liens is equitable relief – as the Participating Noteholders argued in their post-trial brief – not legal relief and could thus only be achieved if the high bar for some kind of equitable relief, like equitable subordination under 510(c), or other equitable contract remedy has been met (which it hasn’t).

Kirpalani’s point is that the Bankruptcy Code ties the hands of Judge Isgur and although there are some options available to him, he doesn’t have the authorization for some split-the-baby resolution to “do justice” as he sees fit that has no real precedence. To which Judge Isgur said, “We may have a more flexible Code than what… people may not have done something before, that doesn’t mean they didn’t have the authority to do it… do I have the authority to do anything other than legal relief.”

In the end, Judge Isgur grew a bit frustrated (maybe more than a bit) that Kirpalani was so adamant that liens couldn’t be restored because that would be equitable relief, not legal relief, and that he believed Judge Isgur doesn’t have the ability to provide this kind of equitable relief under the Code, finally saying “Why does the estate [Incora] care?”

In other words, “Why are you fighting Silver Point and Pimco’s fight here? What’s it matter to you what your pre-reorg capital structure for Plan purposes looks like?” to which the answer, of course, is that the estate doesn’t care too much as long as this doesn’t throw the pre-existing Plan that’s been gathering dust on the shelf into a state of disarray as it needs to be reconstituted for a new capital structure dreamt up by Judge Isgur. Since this would (obviously!) further delay an already much delayed exit from bankruptcy (which, uh, is exactly what’s about to happen…).

After some more model talk – in which, once again, Judge Isgur had to clarify his model creates some kind of pro-rata style transaction – not for the last time Judge Isgur made it clear that this is all about fairness: “There’s no way that the result of this trial, if it turns out that the additional 2026 Notes was impermissible, is going to… merely give an unsecured claim to the claimant… that will not be the result… I will find a way that that is not the result… that would be the worst possible thing I can do,” and “…you’re going to leave here somehow with an adjustment in the capital structure so that you can do a plan. And if I don’t adjust the capital structure, you can’t do a plan. I’m not going to at all say what your plan will be, but it will have to live with whatever the declared capital structure is.”

But this was all a prelude to the primary show: Heidlage, counsel for Silver Point and Pimco, dazed and confused, having to argue against something he didn’t anticipate would be discussed at this hearing (or ever...). “I think that I haven’t had a chance to fully think this through, because that’s not the relief that I think has been sought in this case and I haven’t had… it wasn’t in the briefing. I do want a chance to fully brief it. I will tell you that’s not my understanding of what relief is available to the Court. I do want to take it very seriously. I want to think about it…”

Once again, Judge Isgur made it clear: he wanted to know if everyone thought he had the authority to “interpose equitable relief” on top of legal relief, and if those he’s providing the benefit of equitable relief to (Silver Point and Pimco) don’t want it, then that’s fine and he won’t worry about the fact that granting “legal relief” (the restoration of the liens on the 2026 Notes to what they were pre-transaction with the new-money from Silver Point and Pimco being treated as a worthless unsecured claim) seems unfair to him.

This put Silver Point and Pimco’s counsel between a rock and a hard place: because, on the one hand, they want to reserve their right to appeal something that is, in everyone’s view, a novel extension of how capital structures can be rejiggered post-filing. But, on the other hand, Judge Isgur is offering them something (this equitable relief concoction) that’s not too bad of an outcome and is far preferable to the ~$250mm that was put in going up in smoke through its treatment as unsecured. So, we bore witness to the squirming in real time as this calculation was worked through.

And it was at this time that Judge Isgur – perhaps frustrated by the lack of enthusiasm for his equitable entreaties – started to be a bit more clear. Because it seems throughout the hearing that people were so thrown off kilter that the core contention of Judge Isgur was being missed: the issuance of the additional ~$250mm in Notes that was the first step toward the impermissible uptier, in Judge Isgur’s mind, was unauthorized because it automatically led to the impermissible uptier. The whole transaction – from start to finish – was unauthorized, and as such the additional 2026 Notes will not be pari to the pre-transaction 2026 Notes that have had their liens restored; they’ll be an unsecured claim that will (of course) recover nada (or near nada...).

Heidlage: “…just to be clear, and here, at this point, just to be honest with you, I’m trying to make sure I understand where you’re thinking. So, for example,…”

Isgur: “My thinking is very clearly that I’m going to just leave their lien in place in the first place.”

Heidlage: “But I don’t understand why the 250 that comes in is not at least pari as additional 2026 Notes since,…”

Isgur: “Because the 250 coming in was authorized with an illegal agreement and therefore not authorized. As I found yesterday, your argument that you could have interrupted by that - someone else could have interrupted by withdrawing signatures, is wrong, and that means, and I’m going to tell you, I’ve now concluded with a high degree of certainty, and it’s going to be in the opinion, that the new-money came in unauthorized.”

And the death nail from Isgur: “So now what do you have? They [Incora] did get the money, but they [Silver Point and Pimco] didn’t get anything for it. They therefore have an unsecured claim. Good luck. I think that’s totally unfair. But that’s what your clients [Silver Point and Pimco] did. They advanced 250 under the agreement. Silly. If you think that they win because of that, then you haven’t practiced before me very much, and you have practiced before me a lot.”

With that, the conversation turned to when everyone (e.g., the debtor, the Non-Participating Noteholders, and Silver Point and Pimco) should file briefs on the narrow question of if Judge Isgur has the authority to temper legal relief (which he considers to be the restoration of the liens on the 2026 Notes) with equitable relief (vault the otherwise unsecured Notes that resulted from the new-money injection by Silver Point and Pimco up to pari status to the pre-existing 2026 Notes and then do some kind of retrospective adjustments to achieve some kind of fairness due to the fact that this new-money was injected).

There’s no doubt that the mood shift that occurred with Judge Isgur through the hearing was because of his surprise that he wasn’t welcomed as a liberator, but rather was somewhat condescended to about how wide his remit was in terms of reconfiguring capital structures (especially due to his reliance on a case from 1939 – that some at the hearing kept mispronouncing because they weren’t too familiar with it – to do what he thinks is best...).

On July 3rd we received the responses to the Court’s questions, and to the surprise of no one it was short and sweet from Silver Point and Pimco – basically saying, “We still think what’s contemplated here is equitable relief all the way down, so if equitable relief is pursued then, sure, like, it should be fair to us too. But, at the same time, we don’t think equitable relief is permitted here because of the legal relief (money damages) that’s available – so, we’ll stay mum and reserve our right to appeal. Thx.” (Here's the response from the Non-Participating Noteholders, agreeing with Judge Isgur's views, of course.)

Incora’s Oral Ruling: Fanciful Fairness

Judge Isgur, perhaps chided by the lack of reception to his retrospective capital structure rejiggering or perhaps wanting to keep everyone on their toes, dropped a somewhat ambiguous oral ruling on July 10th – which will be superseded by a written opinion sometime in the (near) future – that wasn’t, at least in full, consistent with his musing from June 26th.

The three principle rulings are as follows. First, the “rights, liens, and interests” to the benefit of the 2026 Notes as they were on the day prior to the uptier exist now (in other words, the liens were not stripped). Second, the selection of the 2027 Notes that were allowed to participate in the 1.25L uptier was impermissible (in other words, Platinum erred, as most thought was liable to be the outcome here). Third, there’s no relief for the 2024 Notes (in other words, since Silver Point and Pimco did have a supermajority in the 2024s, their liens could be stripped).

Judge Isgur then went into a rather long digression on the growth of the leveraged loan market – even though we’re talking about bonds here – before then providing a basic rundown on uptiers.

However, Judge Isgur made sure to emphasize in this preamble that this decision has nothing to say on uptiers more generally – it has to do, as I said before, with the way in which Silver Point and Pimco created the conditions to effectuate the uptier. “This case, or I should say, maybe more importantly this decision does not challenge the legality of uptiering transactions. And for good reason, parties are free to contract and take risks within their contracts.”

After this began the history of how Incora’s transaction came to be – almost all of which was covered in my prior Incora posts. However, there are a few things to note...

First, as is typical, the transaction that was consummated on March 28th began being contemplated far earlier – with Silver Point, which had been a large holder for some time, beginning to seriously think about a non-pro rata uptier in Q3 of 2023, and with their intention always being that they’d cobble together some group that would hold a supermajority (66.67%) of both the 2024 Notes and the 2026 Notes.

In other words, there was never an intention that the transaction would require having to go through the additional step of first manufacturing a supermajority in either the 24s or the 26s – it was always presumed that participants in the transaction would “organically” hold the requisite majorities to strip the liens of the 2024 and 2026 Notes and then vault themselves up into higher priority.

Second, it was a few months later, as liquidity began to become even more stretched, that Incora (PJT) and Silver Point / Pimco (EVR) began trading terms sheets back and forth on the hypothetical uptier…

It was toward the later stages of this timeframe, on Feb 7, that Debtwire reported that an uptier was being contemplated. This then created (although it began a bit before) the perplexing price action that saw the 2026 Notes trade up to over par (and above the inside maturity, the 2024 Notes) as folks began to realize that i) Silver Point and Pimco didn’t have a supermajority in the 2026s and ii) that the transaction could be blocked (this price action was driven primarily by a few funds like Golden Gate that opportunistically started purchasing whatever 2026s they could get their hands on).

At this same time, Incora’s financials were growing more and more precarious as its factoring agreement with Katsumi was pulled and it had to pay back millions under the agreement. This, when combined with its pre-existing level of cash burn, then led to concerns that it couldn’t meet its May 2022 interest payments. To add even more fuel to the fire, there was also a concern (more of a fact than a concern) that they’d receive a negative audit result in the UK unless they scraped together $200-250mm of fresh liquidity and if this were to happen it'd lead to a default under their ABL. In short: they needed a liquidity infusion soon, and it needed to be in the $200mm+ range net of fees.

Against this backdrop, in late-Feb, final terms were agreed to on the Silver Point and Pimco transaction...

However, as holders on the outside looking in finally began to come to terms with what was about to happen, they organized with Akin and PWP to make a last ditch offer that (ostensibly) would provide ~$250mm in new-money like the majority proposal did.

But the issue here – no different than the issue that impacted Angelo Gordon, et al. in Serta – is that it’s hard for a minority group to offer pro-rata solutions that approximate the value to the company that a majority group that’s offering a non-pro rata solution can.

Because, as I’ve harped on, if you’re part of a majority group that’ll enjoy significantly enhanced economics – through shifting value from those left behind – then you have greater flexibility to kick back some of those economics to the company (through lower rate, higher new-money contributions, discount capture, etc.) than a minority group does.

Further, when a minority group tries to pitch a pro-rata solution – as we discussed in Serta – there better be a compelling reason for the majority to go along with it, because the economics to the majority group (almost per se) will be more favorable under their non-pro rata solution than under a pro-rata one.

Anyway, here’s how the proposals – assuming one wants to treat the minority group proposal as viable to begin with – compared. Even without the majority group coming back to make some concessions to become more competitive, it’s clear they already had the most competitive proposal (not to mention the majority were the only ones who put together an executable or even sensical proposal – but I digress).

The final agreed terms of the majority group were, of course, different than how they began in one critical respect: due to the recognition that they didn’t have the supermajority under the 2026s (they did under the 2024s) they would need to manufacture consent and make the transaction multiple distinct steps – and this is where the trouble began.

How this consent was manufactured was simple enough and, in case this monologue is hard to follow, this manufactured consent is the primary issue in Incora’s case and is what really matters. So, here are the steps:

First, on March 28, 2022, a simple majority consented to amend the 2024 Notes, 2026 Notes, and the 2027 Unsecured Notes through the Third Supplemental Indenture that allowed for the issuance of $250mm of new 2026 Notes.

This isn’t controversial. Everyone knew this was a possibility – it was reported on, and Golden Gate, JPM, etc. all recognized that either i) Incora could use its modest pre-existing basket capacity for pari issuance of $75mm without the need for an amendment or ii) those that held a simple majority could amend the basket capacity to create more room for pari issuance (whether that’d be $100mm, $200mm, $300mm, etc.). In short, the consent thresholds to allow for additional issuance (50% + 1) don’t lurk in the shadows of an indenture, and everyone knew this additional issuance could occur.

Second, with the amount of capacity now increased, Incora and certain Participating Noteholders (a.k.a. Silver Point and Pimco) executed the Note Purchase Agreement that issued $250mm of 2026 Notes at par to the Participating Noteholders. Even though some tried to kick up some dust about this aspect of the transaction, it likewise is pretty uncontroversial.

Third, with the Participating Noteholders now having a supermajority of the 2024 and 2026 Notes (since all the new 2026 issuance was allocated to them) all the indentures were amended again – this time pursuant to the Fourth Supplemental Indenture – which stripped the liens of the 2024 and 2026 Notes, allowed for the issuance of new senior debt, and permitted the exchange to occur.

This permitted exchange was then immediately consummated after the execution of Fourth Supplemental Indenture through the Exchange Agreement. And this exchange, of course, involved the Participating Noteholders’ 2024 and 2026 Notes being exchanged into new 2026 1L Notes and the majority of the Unsecured Notes (inclusive of those held by Platinum, Incora’s sponsor) being exchanged into new 1.25L Notes. With the end result being that the Non-Participating Noteholders were left with a handful of dust (now unsecured notes, since their liens were stripped, residing behind an almost insurmountable wall of secured debt)…

So, what’s the issue here? Well, Silver Point and Pimco don’t think there is one, and despite the tens of millions in litigation expense on this issue over the last few years there’s a pretty simple story to tell when the sideshows are stripped away: everyone agrees that a simple majority was required to issue new 2024 or 2026 Notes, everyone agrees that a supermajority could strip the liens of the 2024 or 2026 Notes, and everyone agrees that Incora could enter into private transactions with third-parties when it came to the issuance of new Notes.

Note: Since the issues around the 1.25L uptier vis-à-vis Platinum’s participation are a bit of a sideshow, we’ll largely ignore that. I think it’s pretty clear that Judge Isgur was right that it was impermissible, and I think it’s pretty clear that Platinum knew this too. Platinum was just banking on the fact that the small stub left that’d litigate over their actions could be settled with before push came to shove in court (if no one litigates over the issue, then it’s not an issue…).

As I mentioned back in 2022, and as bore out, the core issue here is over whether the transaction should be treated as a series of discrete steps (all that are allowed under the indentures) that happened to have happened in quick succession or as one integrated transaction where all the “steps” effectively happened simultaneously.

Because, if the latter is true, then the consent threshold to release the liens based on the Notes “then outstanding” (e.g., outstanding prior to the liens being stripped) would be calculated before the Third Supplemental Indenture when, of course, Silver Point and Pimco had a supermajority in the 2024 Notes but not the 2026 Notes.

Whereas if one treats the additional issuance as one discrete step, followed by the lien stripping step thereafter, then a supermajority of both the 2024 Notes and 2026 Notes “then outstanding” would be held by Participating Noteholders before the actual lien stripping step occurred. Therefore, there’s no issue.

What seems to have moved Judge Isgur to the “integrated transaction” side of the argument most is the “have the effect” language around lien releases in the indentures of the 2024 and 2026 Notes – which, as Rosenbaum shows below, is language that isn’t found in all indentures.

In other words, the issue is that if the Third Supplemental Indenture – which allowed for the $250mm in new 2026 Notes, but didn’t strip the liens of the pre-existing Notes – had the effect of stripping the liens, then the transaction is impermissible since the Third Supplemental Indenture was not consented to by a supermajority of the 2026 Notes.

But, if we’re to read contracts within the four corners of the docs, then how can it be that the Third Supplemental Indenture – which allowed for the issuance of some new Notes – had the effect of stripping the liens when it says nothing about, like, stripping liens.

Well, here’s the answer: “The record is clear, and the parties do not dispute that prior to the March 28, 2022, transaction, the Participating Noteholders did not have this two thirds vote to amend the indenture. The Court is limited to the four corners of the documents in interpreting an ambiguous contract. However, whether the Third Supplemental Indenture had the effect of releasing collateral from liens is not a matter of contractual interpretation. It is not possible to determine what effect the amendment had without looking beyond the contract to the surrounding circumstances. The Court must consider the environment in which the third amendment was executed. That environment is one of the domino agreement.” (Emphasis added.)

Dominos and the Downfall of an Uptier

In Judge Isgur’s telling on July 10th, the story of Incora’s transaction is defined by its automaticity: once the first domino fell (the Third Supplemental Indenture) the chain reaction that followed could not be broken by anyone, for any reason, thereafter.

So, the Third Supplemental Indenture triggered the Notes Purchase Agreement which triggered the Fourth Supplemental Indenture which triggered the Amended and Restated Notes Security Agreement (that granted security interests to the new 1L Notes, and released the security interests of the pre-existing 2024 and 2026 Notes) which triggered the Exchange Agreement.

Were there a bunch of separate “steps” between the Third Supplemental Indenture and the Exchange Agreement? Sure. But if those “steps” were automatic, and could not be stopped once the first one started, then effectively there is just one step between the Third Supplemental Indenture and the Exchange Agreement. And since Participating Noteholders didn’t have a supermajority of the 2026 Notes before the Third Supplemental Indenture, and the end result is that Non-Participating 2026 Noteholders had their liens stripped, the transaction is impermissible from start to finish.

To support this view, Judge Isgur points to the fact that all the parties had fully executed documents for the transaction before the March 28 closing call. The closing call was completely scripted, lasted 10 minutes, and was meant to confirm that everyone was ready to close and release their signatures in the preordained step-by-step order without “…any further action by any party”.

Then when the closing call came to a close, at 8:25AM, the Third Supplemental Indenture signatures were released and it was executed, and this was followed immediately by the execution of the Notes Purchase Agreement. One minute later, at 8:26AM, Silver Point and Pimco’s council confirmed the release of the funds from escrow and the signature pages. The exchange-related documents were then released without further action once the Notes Purchase Agreement was executed, and as such the chain reaction continued until 8:53AM when everyone confirmed that the transaction had closed. (There’s some dispute about the timelines here and if some quickly done emails constitute proof of a step being complete – but what’s not in dispute is that the whole transaction, from soup to nuts, occurred within a day.)

Thus, to Judge Isgur’s mind, “The Third Supplemental Indenture had the irrevocable effect of releasing collateral and liens, the two-thirds vote provision was thereby triggered as a consequence of the effectiveness of the Third Supplemental Indenture.”

In other words, it didn’t matter that the Third Supplemental Indenture didn’t strip liens itself, we need to look to what the Third Supplemental Indenture was: the first domino that was tipped over and that led inexorably to the stripping of the liens. The Third Supplemental Indenture had the effect of stripping the liens because of the inexorable nature of how the transaction was executed.

And it’s through this logic that we end up with the declaration that the liens on the 2026 Notes, as they existed the day prior to the transaction, remained in full force and effect the day after the transaction. This includes, of course, Silver Point and Pimco’s 2026 Notes, which were around 59% of them pre-uptier.

Likewise, it’s through this logic that we end up with the declaration that the new 2026 Notes that were part of this integrated transaction were issued, sure, but were unauthorized since they were apiece of this integrated transaction – and thus should be treated as unsecured unless some equitable remedy is applied to their benefit (this was what confused Kirpalani and Heidlage so much on June 26th where they, reasonably, assumed that the additional 2026 Notes would of course be pari to the other 2026 Notes even if the subsequent uptier component of the transaction was deemed impermissible).

But, at the same time, through this logic we also end up with the declaration that since Silver Point and Pimco did hold a supermajority of the 2024 Notes before the Third Supplemental Indenture, that lien stripping was permissible and thus no relief is granted.

In a demonstration of unparalleled understatement, especially based on what was discussed on June 26th with all the recap rejiggering talk, Judge Isgur concluded the oral ruling by stating, “I know this opinion is probably not what anyone expected, so I’m going to ask the parties promptly to file a request for a hearing if one is required and the parties cannot agree on remaining issues to be decided. In the meantime, I’m going to hold to the expectation that the debtors are going to go ahead and proceed now to act on what their capital structure has now been declared to be.”

So, with that, Incora’s uptier was upended – with not a mention of Judge Isgur’s Excel model and all its inputs or, for that matter, the $250mm new-money contribution by Silver Point and Pimco (which, by omission, was assumed to be relegated to an unsecured claim).

This, to be fair, was what Judge Isgur warned when he became a bit hot under the collar earlier: if you don’t want his benevolence, then you’re not going to get it. So, Silver Point and Pimco donated $250mm, extended Incora’s lifeline by a few months, and have been left with little to show for it – except that because of what the capital structure was assumed to be at filing, Silver Point and Pimco provided the DIP, chalk full of fees, which Judge Isgur made clear does stand (despite protestations from the Non-Participating Noteholders in light of the oral ruling).

And that’s the problem with equitable solutions: how do you truly roll back to time zero, when all that’s happened since is predicated on what occurred after time zero. It’s hard to imagine, and then effectuate, what can be unburdened by what has been.

Attenuated Assumptions on Automaticity

How we ended up here begins and ends with fairness, and the attenuated assumption that the domino agreement was not a result of, like, trying to make the transaction as logistically efficient as possible, but rather was a deliberate effort by Silver Point and Pimco to put Incora into a vice grip that they could never wrestle free from. Because, the thinking goes, otherwise the whole transaction wouldn’t make sense to Silver Point and Pimco.

And, look, two things can be true at once. It can be true that the mechanical process – as Judge Isgur illustrated with his timestamps – was the most efficient manner to effectuate the transaction and that Silver Point and Pimco thought it made it hard (but not impossible) for Incora to back out of (e.g., Incora would find it difficult to allow the $250mm in new 2026 Notes, obtain the funds, and then basically say, “Uh, not so sure about this exchange agreement we’ve all agreed to now – let’s get back to the bargaining table for some edits.”).

I’ll leave all the technical arguments around how the escrow terms, signature releases, etc. made the transaction impossible to squirm out of to others. Because what seems clear from the oral ruling – both in its emphasis and its structure – is those arguments were escape hatches for Judge Isgur to utilize because he thought that, at base, there was no way that Silver Point or Pimco would do this transaction if there was the possibility it wouldn’t be seen through to the finish once it started.

In other words, it’s clear to Judge Isgur that the transaction could only ever make sense, and would only ever be consented to by Silver Point and Pimco, if it were under the “automatic” process that occurred (at one point he did seem to concede the transaction might not have been inevitable in a literal sense once it began, but was asymptotic to inevitable which was good enough for him).

“Pimco and Silver Point only offered the new $250mm on the contingency that the entire transaction would take place. Pimco and Silver Point were unwilling to provide new-money on a pari passu basis. Rather, they expected super senior first lien debt. The transactions would not have worked from Silver Point’s perspective without elevated lien status, because the Participating Noteholders were providing new-money at a lower interest rate than they would have lent it if the new-money were issued on a pari passu basis.”

But there are a bunch of conflations here. Sure, Silver Point and Pimco had the desire to make the transaction have the appearance of being binding to try to ensure that the transaction, in its full form, did occur. And there are emails that appear damning on the surface to this end – but these should be read from a posturing perspective (e.g., we expect this to occur) than a definitive perspective (e.g., this must occur).

However, the broader idea – and this should be the takeaway for readers, not the babble that’s led up to this – is that Silver Point and Pimco i) did undertake the transaction with the suspicion that the football could be yanked away from them as they went to kick it and ii) did, as anyone would, want to minimize the probability of this happening but would have executed the transaction even if this probability were far larger than they suspected it was.

But the unmistakeable impression that one had through the entire Incora trial is that Judge Isgur doesn’t believe that this transaction could have occurred if there were a 2% probability, never mind a 20% probability, that the new-money lent in return for the 2026 Notes (at par!) would not have led – as if by a sequence of inexorably falling dominos – to the uptier.

And it’s because of this that we have the escape hatches of the “have the effect” language linked to the dubious signature release arguments, etc. used to render the transaction “automatic” in nature and thus unauthorized.

In short, the transaction is unfair because it was automatic and never would have happened if it weren’t automatic. But it wasn’t automatic (in my view, and that of Silver Point and Pimco) and even if it were automatic in this instance, it doesn’t negate the fact that if it weren’t automatic (perhaps even if it weren’t likely that the new-money put in for the new Notes would lead to some pre-negotiated uptier) that the transaction would still make sense under most circumstances from the Silver Point and Pimco vantage point, and would have been done (albeit it would’ve been riskier).

And if one takes this latter argument on faith, then it begins to bite back on if it matters that this transaction had the patina of automaticity when it would have been executed regardless of it were automatic within any reasonable definition of the term. The fact there aren’t contemporaneous emails to that effect is a reflection not of evasion, but rather of a truth so self-evident it doesn’t need to be stated (plus, it didn’t need to be contemplated since the steps weren’t seen as a huge issue if executed in a deliberate sequence, as they were...).

In the end, as in all transactions, one can make a downside case, a base case, and there’ll be some probability that can be assigned to the downside case that makes the transaction breakeven from a desired IRR perspective.

For Incora, the calculation is pretty straight-forward (or, perhaps better said, to illustrate my point directionally we can make it pretty straight-forward). Think about it from a simple waterfall perspective and under a hypothetical transaction structure that is not, under a reasonable interpretation, automatic (e.g., there’s a lag between the additional issuance and the eventual uptier, or a clear and self-evident circuit breaker that Incora could hit).

Each of Silver Point and Pimco based on their current holdings, the purchase price of those holdings, the coupons they’ve clipped to-date, etc. would be looking at some return based on some valuation of Incora. In the downside case, if they invest $250mm for new 2026 Notes and Incora doesn’t move forward with the hypothetical exchange, then their 2026 Notes would be pari to the pre-existing 2024 and 2026 Notes in the waterfall (they would inarguably be pari in this case since they aren’t wrapped up in some domino agreement) and will dilute down the recovery in percentage terms (same numerator as we’ll assume a normalized valuation, higher denominator) and thus will crystalize a non-trivial loss (since the Notes were purchased at par and the recovery will be some number quite a bit below par – the Notes were trading around the 80s pre-transaction, would trade down on the dilution all else equal, and would likely trade down further if it became clear that filing was going to occur).

While no one can know what future recovery levels will be with any real certainty, there is a known structure to the downside: it’s whatever you’ll lose on your existing holdings based on your purchase price of those holdings plus whatever you’ll lose on your new-money contribution. Sensitize this all to the ends of the earth, predict a higher or lower valuation for Plan purposes, predict a longer runway (more coupons pre-filing) or shorter runway (less coupons pre-filing), etc. but the rough structure of the downside is the same.

Likewise, the base case – where the uptier does occur in the future – will have a similarly known return structure (although there are more elements that feed into the structure). There’ll be the coupons that’ll be clipped pre-filing, the recovery on the now senior debt held, and whatever added economics result from almost certainly providing the DIP if the company ends up filing in the future.

In this kind of situation, there will be – almost irrespective of what value we assign to Incora – an asymmetric quality to the return structures. The downside case will be somewhat capped because your (negative) return is being driven primarily by diluting down your pre-existing holdings and the premium paid for these additional Notes. However, in the base case you’re shifting significant value to yourself – as illustrated in the original Plan filed by Incora (which assumed that the transaction was valid) where 96.5% of post-reorg equity would flow to Silver Point and Pimco plus $420mm in take-paper paper. And, because of their presumed position in the capital structure at the time of filing, they provided the DIP that will result in $324mm of exit notes too.

So, to back up again, it’s of course the case that the transaction could still be done even if there were some probability, remote or otherwise, that the exchange step(s) wouldn’t happen after the issuance of the new 2026 Notes. What the probability that makes the transaction make sense to still do would be contingent on the factors above – but it’d be somewhat high.

Indeed, this is all understating the case for moving forward with the transaction regardless of if the uptier occurs as contemplated pre-transaction. Because even if the issuance of Notes occurs, but Incora decided to walk on this exchange, Silver Point and Pimco would still be left with a supermajority in both the 2024s and 2026s.

So, even if their initial uptier plan didn’t pan out for whatever reason, they’d still have manufactured a dominant bargaining position. Maybe the terms of a future transaction wouldn’t be as favorable but remember the context here: Incora needed cash to avoid a negative audit result, to meet its May interest payments, etc. and it was likely they’d need additional liquidity in the future even after the infusion from the new 2026 Notes. (Even if they didn’t need additional liquidity in the future, Incora would be in a position to obtain a bit of discount capture and reduce its cash interest through doing an uptier with Silver Point and Pimco, so it’d still make sense for them to engage in discussions on it even if they had appeared to right the ship due to the initial liquidity injection.)

Therefore, even if Incora came back to drive a “hard” bargain after the additional Notes issuance, Silver Point and Pimco are still in a strong position. And if this initial infusion wasn’t sufficient, and Incora approached the precipice of filing again, they’re not in a position to extract too much more from Silver Point and Pimco sans threating to take the company into Chp11 where the downside case would be crystalized for Silver Point and Pimco (as it would be for Platinum, the sponsor, too…).

Further, not to head down too much of a rabbit hole, but if you’re designing an initial notes issuance that’s not contingent, in the literal sense of the word, on a future uptier then you could change around the terms a bit to make it such that a “carrot” still exists for a future uptier (e.g., providing the bare minimum of liquidity needed to obviate the negative audit result through the new Notes issuance, but then coming back a short while later and saying if we do an uptier we’ll inject another $[xx]mm, lower cash interest on the new debt, exchange at a discount, etc.).

The fact that the transaction structure was structured how it was is because no one saw a large issue with it – there was no need for obfuscation of the real intent here because there wasn’t the belief that anything needed to be obfuscated. If there was a significant belief that there was an issue, then the same result (sans automaticity, depending on how one defines that…) could have been achieved.

Again, what probability of the uptier happening within close proximity (however one defines that…) of the Notes issuance would make sense for Silver Point and Pimco is a subjective, multi-factor call.

But based on i) the upside economics if it does occur as idealized and ii) the known, calculable downside economics and iii) the fact Incora’s sponsor-backed, everyone knew Platinum wanted to do something to perverse the optionality of its equity, and that something had to be done in the next few months (before April / May of 2022) and that paying a premium for the 2026 Notes (par) to be in the true driver’s seat of future negotiations would probably lead to some kind of non-pro rata transaction that could shift additional value to you (and allow you to provide the DIP should filing occur) all makes it such that what I’ve called the “breakeven probability” (e.g., the probability of being stuck in a pari position with the additional Notes that still, on an expected value basis, makes the transaction make sense to pursue) is pretty high.

(Plus, we’re just assuming in all of the above that there’s no probability that, future uptier or not, after the issuance of the new Notes that Incora wouldn’t turn things around with their now extended runway and that all the Notes wouldn’t trade up and eventually return par! This is an understandable assumption to make in hindsight. But if we imagine ourselves pre-transaction we should assign some non-trivial probability to this happening – keep in mind, Silver Point began buying up $39mm of Incora’s 2027 Unsecured Notes post-uptier, and did so for a reason!)

There’s little doubt that Silver Point and Pimco (obviously!) wanted to minimize the downside risk of Incora pulling out and this led to trying to cultivate the appearance of automaticity but that does not, in and of itself, prove the automaticity. However, to Judge Isgur it does, and to help provide a structured rationale to support this contention we have the escrow and signature release arguments trotted out.

I don’t want to beat a dead horse here (although I've surely already done so by this point). But, to be clear, when Judge Isgur says, “Pimco and Silver Point were unwilling to provide new-money on a pari passu basis.” this is a misconception, and one that was allowed to fester through the whole trial. The whole transaction structure – as occurred in real life and as fleshed out above – is based on a willingness to provide new-money on a pari basis and take a risk that it might remain pari.

Sure, that risk that the new-money would remain pari was viewed as de minimis by Silver Point and Pimco in this case – but the notion that if the probability of the new-money leading to “elevated lien status” through an eventual uptier dipped from 100% (automatic) to 99% or 95% or 90% it would then make them “unwilling” to put in the new-money is illogical on its face. If it made economic sense at 100%, it’ll still make economic sense at 95% -- it’s all about expected value, even if when one begins thinking through all the possible path forwards without the automaticity of the transaction we quickly find ourselves thinking through many, many unique paths (based on what a future transaction that’s not nailed down before the additional issuance would look like) that’d each create unique return profiles.

Domino Deliberations: What Constitutes a Domino?

So, look, if Judge Isgur’s view – and this may or may not be the case – is that Silver Point and Pimco created a domino agreement, one that could not be stopped once it started, and that renders the transaction impermissible but if they had inserted a metaphorical checkpoint at which Incora could’ve untethered itself from the uptier before it was effectuated in a clear and unambiguous way there’d be no issue here then sure, fine, whatever.

In other words, if Judge Isgur’s view is that if all the docs weren’t executed beforehand then this transaction would be permissible in totality – as the steps would all be treated as distinct – there’s not too much to squabble about. It’s a technical ruling that most would then acknowledge is predicated on the fact that Judge Isgur really doesn’t like the optics of this transaction.

However, the broader issue is if we begin to expand the definition of what constitutes a domino due to the “have the effect” language contained in a non-trivial number of indentures. If a transaction is not automatic – for the sake of argument we’ll assume Incora’s was – then under what conditions would the Third Supplemental Indenture still “have the effect” of releasing liens even though it says nothing about releasing liens?

It wouldn’t be the case (?) that if additional Notes were issued to certain funds, a year went by, and then a non-pro rata uptier occurred that was done by a supermajority that was created by dint of the additional Notes issuance that this would be unauthorized. But what about if the timeframe is two months? Two weeks? Two days? Two hours (without all the docs executed beforehand)?

What if there were emails that fleshed out the uptier before the additional Notes were issued? What if there were internal emails that discussed why it made sense to purchase new Notes at par (even though pari notes are trading below par now) because of the value that comes with a supermajority?

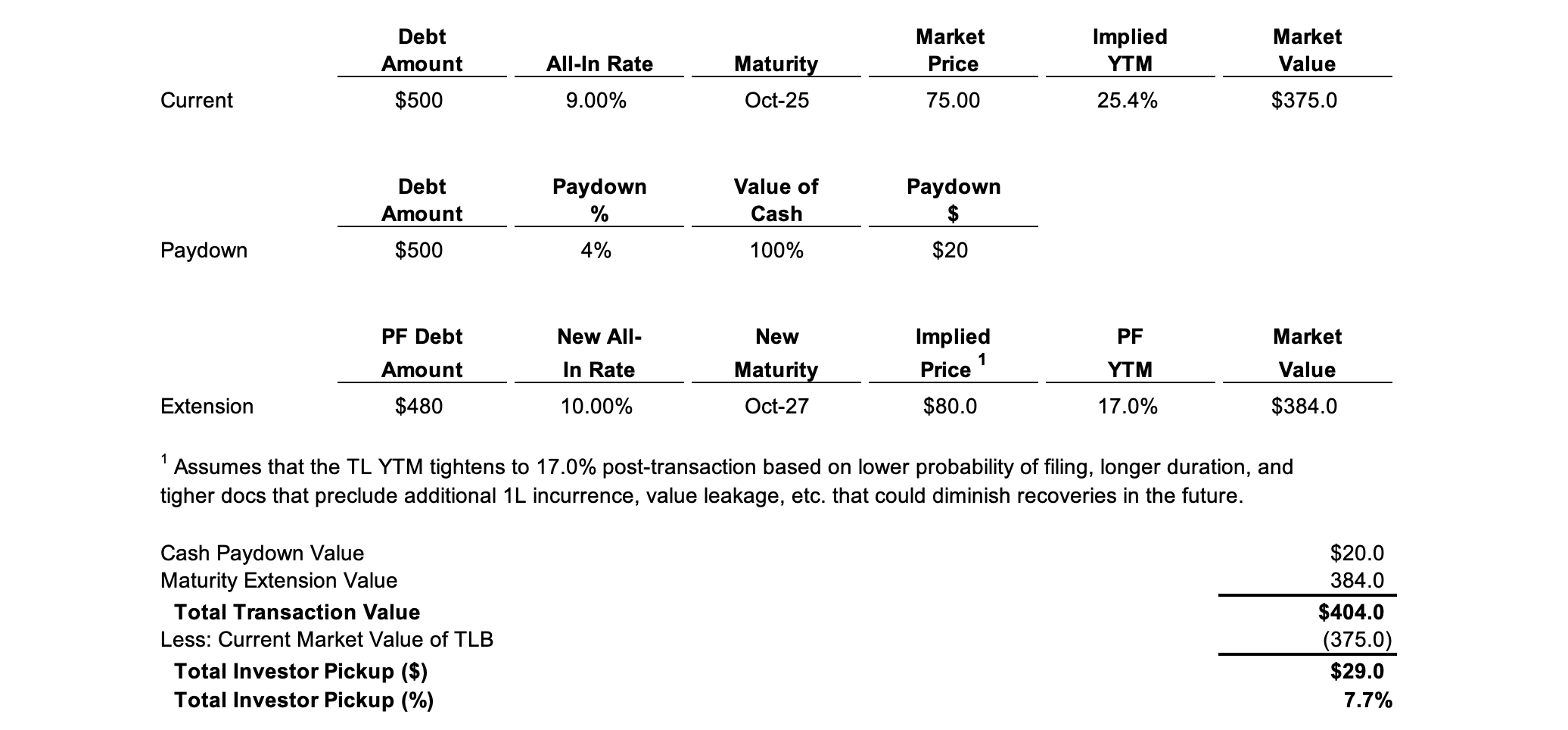

What if there were (gasp) some handwavy investment committee memos that projected out a bunch of inflated IRRs – perhaps based in part on a future filing and being in the position to provide the DIP, etc. – as is inevitably the case in these situations? (For example, below is Invesco’s rough math on Robertshaw – before Canyon, Bain, et al. got wind of what they were doing and manufactured consent in a different way than in Incora’s situation to get back in the driver’s seat after being sneakily kicked out of it by Invesco…).

If the view of the Court is that a domino agreement renders this transaction impermissible due in part to its fundamental unfairness – and unfairness was evoked a lot – then how much is that unfairness really altered when an amendment that leads to additional issuance has a 99% probability, instead of a 100% probability, of then leading to another amendment that strips the liens? What if it’s 90%, 75%, 50%…? And, of course, how does one know the probability to begin with?

This is the quagmire that domino deliberations inexorably lead to: what constitutes a domino that can begin a chain reaction that cannot be stopped? And then how do you handle the aftermath? How do you work your way back up the chain of fallen dominos in the desperate search for a fair resolution unburdened by what has been? And in this fanciful search for fairness, does the party that matters most from a real-world, economic perspective (the debtor) end up bearing the brunt of the fallout through a (much) delayed exit as equitable remedies are mulled over?

Conclusion

So, now the saga that began over two years ago stretches on. While Judge Isgur seemed to think that with his oral ruling Incora’s exit from Chapter 11 would happen lickety-split we will need to continue to wait some more before that occurs.

The written opinion from Judge Isgur still hasn’t arrived – to be honest, there’s a lot that wasn’t articulated in the oral ruling that really should be clarified in the written opinion – and now everyone is back at the table to reconfigure a Plan based on the capital structure as dictated from on high (here it is, over a month after the oral ruling).

With no one in as much of a driver’s seat after the oral ruling it was inevitable there’d be some new fights – some of which probably surprised (read: irritated) Judge Isgur. For example, the major development in the few weeks after oral ruling involved Non-Participating Noteholders fighting the permissibility of the DIP from Silver Point and Pimco since, like, it is consistent to think that if their actions pre-filing were impermissible, and there are benefits that accrued to them post-filing (being in the best position to provide the DIP) because of those actions pre-filing, then the post-filing benefits should be open to question.

Judge Isgur said at the close of the trial, in defense of restoring the liens of the pre-existing 2026 Notes, that he doesn’t want Silver Point and Pimco to “…get the entire benefit of their bargain knowing that they cheated...”. Well, if the DIP remains – and the DIP was a consequence of the priority enhancement inherent to the impermissible transaction – then Silver Point and Pimco are getting some of the benefit of having “cheated” as the Non-Participating Noteholders have been quick to point out (true, not the entire benefit – but what about fairness?).

Judge Isgur doesn’t want to hear it. He’s made it clear that the DIP stands. But, in the spirit of ensuring that every equitable stone does not go unturned, he’s now heard about it. And all the while Incora itself – since it’s worth remembering there is a company that, like, sells stuff, has employees, has contracts, etc. – has been left in the lurch to wait it out.

This is the domino theory at work. In a desperate and, to be clear, good faith attempt to create the most fair outcome – even though the actual “fair” outcome as detailed in Judge Isgur’s oral ruling doesn’t align with what he thought the initial most fair outcome would be on June 26th – a series of unintended quagmires have now cropped up in the rice paddies of the Southern District of Texas.

Note: Here’s the latest Plan that takes into account Judge Isgur’s capital structure rejiggering – more or less in line with the earlier Plan, but with the composition of holders in some classes of course changed around and the additional 2026 Notes (termed the New Money Unsecured Notes in the Plan, which is a more accurate description of what they've been deemed to be) that arose from the transaction to manufacture the supermajority relegated to the back of the line with a recovery comprised of 1.4632% of post-reorg equity (subject to dilution).

]]>